A sound portfolio construction process is critical to avoiding the pitfalls of behavioural biases, which will become all too apparent as the credit cycle turns

4 minute read

Has the decades-long bull market in bonds made some credit managers look better than they really are? In the favourable market environment of the past 30 years, many managers found success simply by taking on additional risk and not necessarily adding much value.

When evaluating credit managers, it is necessary to measure how their strategies are likely to perform over the course of a full credit market cycle. If a manager maintains a long credit risk position at all times, through periods of both tightening and widening credit spreads, its ability to add alpha is questionable. The true test of a credit portfolio strategy comes when the trend shifts - an increasing possibility as interest rates rise from historically low levels and credit spreads begin to show much higher levels of spread volatility.

The overconfidence game

Why do many credit managers leave clients exposed to risk by tilting their credit portfolios toward lower-rated issuers? The root of the problem stems from behavioural biases. Specifically, it is virtually impossible to predict systemic shocks to investment markets, and the beginnings of economic recessions are usually acknowledged in hindsight, after the onset of risk asset volatility. This often results in an overconfidence that afflicts credit managers and research analysts (as it does with skilled practitioners in any field), inflating their self-perceived ability to pick winners or encouraging the common misconception that they will be able to get out of the way in advance of systemic shocks or recessions.

This becomes acutely problematic when constructing credit portfolios. Bond fund managers typically look to bottom-up fundamental research analysis for investment ideas to fill their portfolios. But as mentioned, overconfidence and other biases result in credit portfolios that are heavily weighted toward lower-rated and riskier issuers.

This is not necessarily a problem when credit conditions are favorable. But when the cycle changes, many portfolios are vulnerable to a drop in performance. Skilled credit managers will look to temper these potential biases and build a well-constructed portfolio between higher quality and higher risk issuers, in order to deliver positive excess returns for investors during all stages of a full credit cycle.

Tipping the scales

Credit analyst recommendations are forecasts about the direction of credit spreads vs. a benchmark, sector or peer group. Making a positive recommendation on a high-quality bond with a tight credit spread puts an analyst in a difficult spot; the only way that bond would outperform would be if riskier bonds performed poorly. For lower-rated issuers where credit spreads are wider, analysts have more room to make positive recommendations with the benefit of additional spread carry, and those analysts who are bristling with confidence make more of them. If that is the case, it presents a problem for credit managers; a greater number of outperform recommendations for lower-quality issuers skews the list of investment ideas that managers choose from quite significantly.

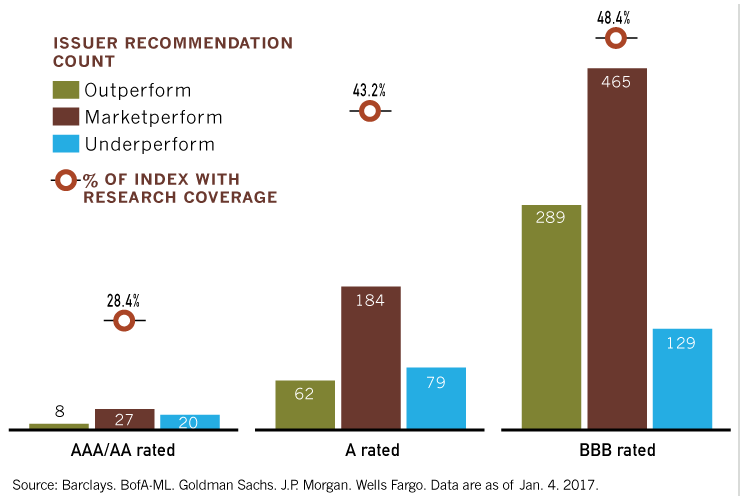

To test this view, we pulled every investment-grade corporate bond recommendation from five publishing sell-side research providers. We found BBB rated issuers get most of the attention from analysts: nearly half of the lowest-rated issuers were covered by research analysts. In the top rating categories, only 28% were covered.

It is true there are more lower quality than higher quality issuers in the investment-grade market, with more than 700 BBB rated issuers vs. about 400 issuers with ratings of A or above. But our analysis confirmed a significant tilt toward outperform recommendations in lower-quality or riskier bonds.

Looking across rating categories within investment grade, outperform recommendations for BBB rated issuers outnumbered underperform recommendations by more than 2-to-1 (289 outperform vs. 129 underperform.) Among higher quality issuers - those rated A or better - the outperform-underperform split was more balanced, with 70 outperform vs. 99 underperform recommendations. And when you compare 289 outperform recommendations of BBB rated issuers to only 70 outperform recommendations on higher quality issuers, the skew toward risky ideas is more than 4-to-1.

Figure 1. Outperform recommendations on lower-quality bonds show optimism from sell-side research departments

For a credit manager looking for ideas in this universe of analyst recommendations, the scales are clearly tipped toward higher risk issues. This can, and often does, result in portfolios that are overweight risky bonds throughout the entire investment cycle.

Carry that weight

The problem of overexposure to credit risk becomes more acute when spreads are narrow (as they have been for some time) and when volatility increases (as began in February.) Exposure to risk that is beyond investors' parameters can be bad, yet this might be passed over by some managers when trends are favorable (i.e., when spreads are wide and it is easier to spot value) and there is yield (carry) to be gained by taking on additional credit risk.

The narrative flips when spreads are narrow, interest rates begin to rise, geopolitical risks increase and we enter the later stages of an economic cycle. The tighter credit spreads get, the smaller the break-even points for adding credit risk get as well, especially at longer maturities where it does not take much volatility to eliminate the yield (carry) premium. The example below, which calculates the spread and break-even points for A and BBB rated issues across different maturities (2- to 30-year), illustrates the potential risk.

Figure 2. The break-even points for adding credit risk get smaller, especially at longer maturities

Given how narrow spreads are in the current cycle, the margin for error to adding credit risk exposure appears very small. It is not that investors and managers should avoid taking on credit risk altogether. Rather, they should view credit risk at longer durations as a precious commodity, seeking it only with those ideas where their conviction is highest. In every cycle over the past two decades, there have been many periods of sudden spread volatility with such magnitude to potentially eliminate carry, most evident in higher risk credits.

Figure 3. Volatility can spike, which has the potential to eliminate carry, particularly in BBBs

Under the influence

It is well understood that sound bottom-up fundamental research is vital to the success of any corporate bond portfolio management process. However, this analysis is meant to highlight a very real behavioural bias that affects corporate credit portfolio management. Skilled managers should be cognizant of the different ways behavioural biases can influence investment decisions and address these biases during the portfolio construction process. Credit managers should ask these critical questions:

1. Are they maintaining balance between higher risk and higher quality issuers throughout the entire credit cycle as to not constantly overemphasize riskier bonds?

2. Do they have an established process to determine when investors are adequately compensated for taking on additional risk — and just as importantly, when they are not?

The second question is important for credit investors to ask of managers when evaluating their track records. Were excess returns generated just by adding risk to the portfolio? If so, that does not speak well to the skill or ability of the manager. Those managers who account for inherent biases through the portfolio construction processes would be in a better position to deliver excess returns over all stages of a full credit cycle.

THIS ARTICLE FIRST APPEARED IN PENSIONS & INVESTMENTS