In our latest real assets update, we check recent trends in UK property and infrastructure equity in a period of Brexit-related uncertainty.

3 minute read

In liquid markets, volatility is up from its recent ultra-low base. The return of global inflation and prospect of tighter monetary policy across the world, trade tensions, Brexit unknowns and concerns about corporate earnings have all played a part.

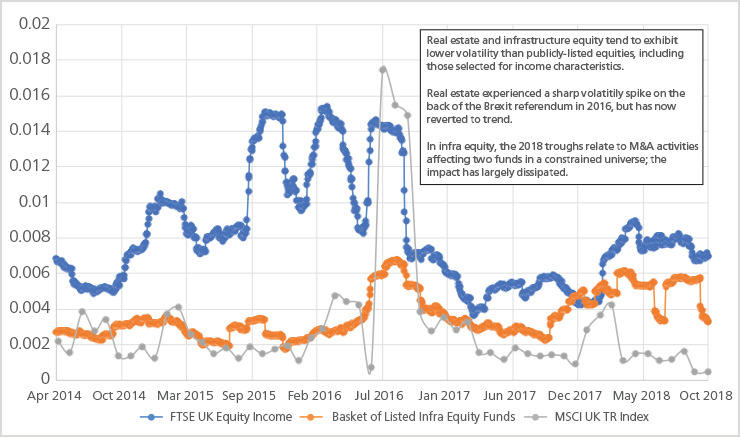

Real estate tends to display relatively low volatility compared with liquid assets (highlighted in Figure 1 below.) Although the unexpected outcome of the Brexit vote in 2016 caused a volatility spike, it has now fallen back to the longer-term trend. We expect the return of volatility to impact real estate and other real assets, but with a lag.

Meanwhile, the search for yield continues to drive activity. Demand for prime assets has forced yields to record lows in most office and logistics markets, and the premium for investing in secondary assets or peripheral locations has been shrinking as well. Trends in the retail sector differ somewhat, with investors increasingly acting with caution as structural challenges become more apparent.

Investors positioning for the next stage of the cycle should look to limit exposure to riskier forms of real estate and focus on core product with defensive qualities.

Figure 1: Comparing quarterly rolling volatility of select liquid and illiquid assets

Infrastructure equity: strong demand continues following record fund raising

In volatile times, we see strong interest in infrastructure, as the provision of essential services continues to be relatively decorrelated from economic fluctuations. Assets with scope for income growth and/or inflation protection are of particular interest in a rising rates environment.

There has been record fundraising in European-focused infrastructure of $32.2 billion in the year-to-date, according to Preqin. Renewables and higher yielding sectors such as full fibre broadband have been hotspots of activity. Interest in the latter has been driven by the digital agenda across Europe, including the UK government’s objective to connect 15 million households by 2025.

Against this backdrop, infra has shown lower volatility than public equity comparators, as highlighted in Figure 1. That includes broad market indices like the FTSE 100, as well as the dividend paying stocks represented in the FTSE Equity Income Index that are often followed for their more defensive characteristics.

Nevertheless, it is important to note the idiosyncratic nature of infrastructure investments, and the nature of risk. For example, the UK government recently decided to phase out subsidies for small-scale solar by 2019, changing the revenue dynamics. In Europe, the trajectory of the renewables market is also shifting towards a subsidy-free environment.

Private assets: checking indicative spreads over comparable government bonds1