In May, our EMD team discusses the most effective way to manage fixed income through episodes of heightened uncertainty.

Read this article to understand:

- What the current uncertainty around trade and tariffs means for EMD

- The importance of staying focused on the risk-reward relationship

- The potential scenarios for some key emerging markets

Welcome to Bond Voyage. Over the last month, our fixed income teams have been kept on their toes by President Trump’s tariff announcements and about-turns, and what they mean for bond markets. They discussed direct effects, second-round impacts, and the possibility of recession in the US.

Among all this uncertainty, they decided to focus on the important point: the need to focus on the most effective way to manage fixed income, particularly emerging markets (EM), through these episodes.

For this month’s newsletter, the EM Debt (EMD) team reflects on this essential matter.

Emerging market debt: Navigating the unknown

Let’s start with what we do know. The current environment is highly complex and uncertain. If you wait for things to become clearer, you could risk sitting on your hands for the next four years. If you believe you can accurately predict President Trump's next move and its short, medium, and long-term implications, at best you might be right on one aspect of the puzzle, but you'll be scrambling to deal with unintended consequences.

To generate alpha, we have to make decisions even when we don’t have enough information. To quote philosopher William James, “When you have to make a choice and don't make it, that is in itself a choice.” But how do you make an investment decision when information is scarce?

Start with what you know: The price

The immediate aftermath of President Trump's tariff announcements and partial retraction reaffirmed our view on the need to always focus on risk-reward.

This means focusing on what you could lose in the worst-case scenario, rather than trying to predict whether it will materialise and risk getting caught in a doom spiral.

By focusing on price, we have concluded that, for some high-yield (HY) names, all but a return to COVID-19 or the depths of the Russia-Ukraine war would see you incur losses over a six-month time horizon. Spreads are not clearly cheap at a headline level and are not clearly pricing in a recession. However, they have widened, with significant dispersion. Focusing on headline levels would ignore opportunities that have been created, particularly in HY.

Stay dynamic, open to a range of outcomes

Investment decisions need to be led by asset prices, with a focus on risk-reward and being dynamic with our risk-taking. Something has fundamentally changed and will continue to shift as the US administration attempts to rejig the global order.

The end of US growth exceptionalism?

Whether this leads to a US recession, how severe it is, and whether ultimately we see a global recession, are open questions. A US slowdown and a move away from dollar assets (so a weaker dollar) could be positive for EM. EM local-currency assets would look particularly attractive.

Local yields could move lower, offering an opportunity. EM inflation could also come down quicker than expected, with weaker growth, lower commodity prices, and the potential for disinflation to be imported from China. Added to this, potentially slower global growth could create an environment where central banks are able to cut rates more aggressively than the market currently expects.

A focus on risk-reward is synonymous with bottom-up credit selection

One need not understand the precise state of the world to gauge a likely direction of travel. To that effect, we took a first stab at sifting through much of the EM universe to try and derive early and potential “winners and losers” from the reciprocal tariffs, knowing full well that we only have a 90-day reprieve.

We took a first stab to try and derive early and potential “winners and losers” from the reciprocal tariffs

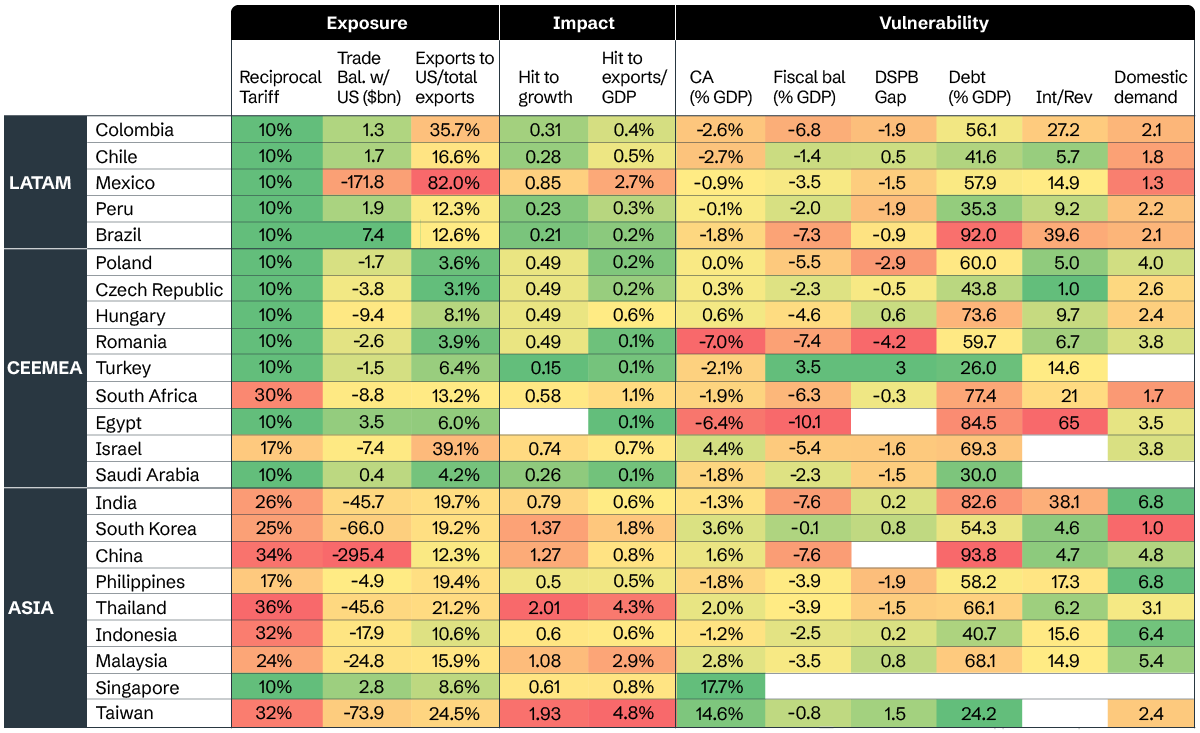

Figure 1 stacks up the exposure and impact of US tariffs against countries’ macro vulnerabilities. Geographically speaking, Asia may bear the brunt of the tariffs if they are reinstated, whereas Latin America looks more insulated given it lies in the western hemisphere and is largely a commodity exporter to the US. Meanwhile, Central Europe, the Middle East and Africa (CEEMEA) are more indirectly impacted, wedged between growth outcomes in both the EU and China.

At the country level, it’s important to remember that in such uncertain environments, countries running large twin deficits, such as Romania and South Africa, are usually more exposed if a stagflation scenario keeps global rates high. On the other hand, those with diversified economies and/or robust domestic demand could fare better, such as Poland, India, and Brazil.

And with so much still unknown, having extra fiscal space always helps – so those with fiscal challenges, such as Hungary and Colombia, may be in for a rougher ride. Last but not least, what side of the geopolitical spectrum a country falls on is increasingly relevant: Mexico, Turkey, and Poland look like winners relative to South Africa, China, and Colombia.

Figure 1: EM exposure and vulnerabilities to US tariffs

Source: Aviva Investors, IMF, National Authorities, April 2025.