Following unsuccessful attempts in the past, the Japanese government’s structural reforms now seem to be bearing fruit. This has contributed to a record high on the Japanese stock-market, but is it sustainable?

Read this article to understand:

- Why Japanese stocks are surging after a long period in the doldrums

- The impact of corporate governance and market reforms on the outlook for Japanese companies

- What this means for the yen

For Japan watchers, February brought some dispiriting, if familiar, news: the economy is shrinking. Following two consecutive quarters of negative growth, the country is now in what economists call a “technical recession”.

Disappointing GDP numbers are not a new phenomenon in Japan, which has long struggled to rouse itself from an economic malaise characterised by deflation and sluggish growth. But look deeper and there is cause for optimism on the Japanese economy, as structural reforms and long-awaited consumer price rises begin to come through, injecting new life into the stock market. These factors help explain why Japan could offer attractive opportunities for multi-asset investors in 2024 and beyond.

The lost decades

For the origins of Japan’s economic torpor, we need to look back to its boom years in the 1980s, when it became a world leader in sectors such as technology, auto and finance. Between the 1960s and the late 1980s, Japanese economic growth was double that of the US.1 Asset prices surged. Prime real estate in the Japanese capital in 1989 was selling for $20,000 per square foot (almost four times as much as the priciest real estate in the world more than three decades later – even before adjusting for inflation).2

But in 1990, a stock-market crash and a knock-on banking crisis, coupled with structural factors such as a rapidly ageing and shrinking population, led to “lost decades” of slow growth and low inflation, turning into deflation in the 2000s. Interest rates haven’t risen above 0.5 per cent since 1995 and have been negative since 2016.3

Both individuals and companies have focused on saving, in part to make up for the lack of returns on their investments, with the unintended consequence of keeping inflation persistently low. The government and Bank of Japan (BoJ), the central bank, have long tried to break this cycle through policies designed to spark wage and price rises – notably under the “Abenomics” reforms of former Prime Minister Shinzo Abe – with mixed results.

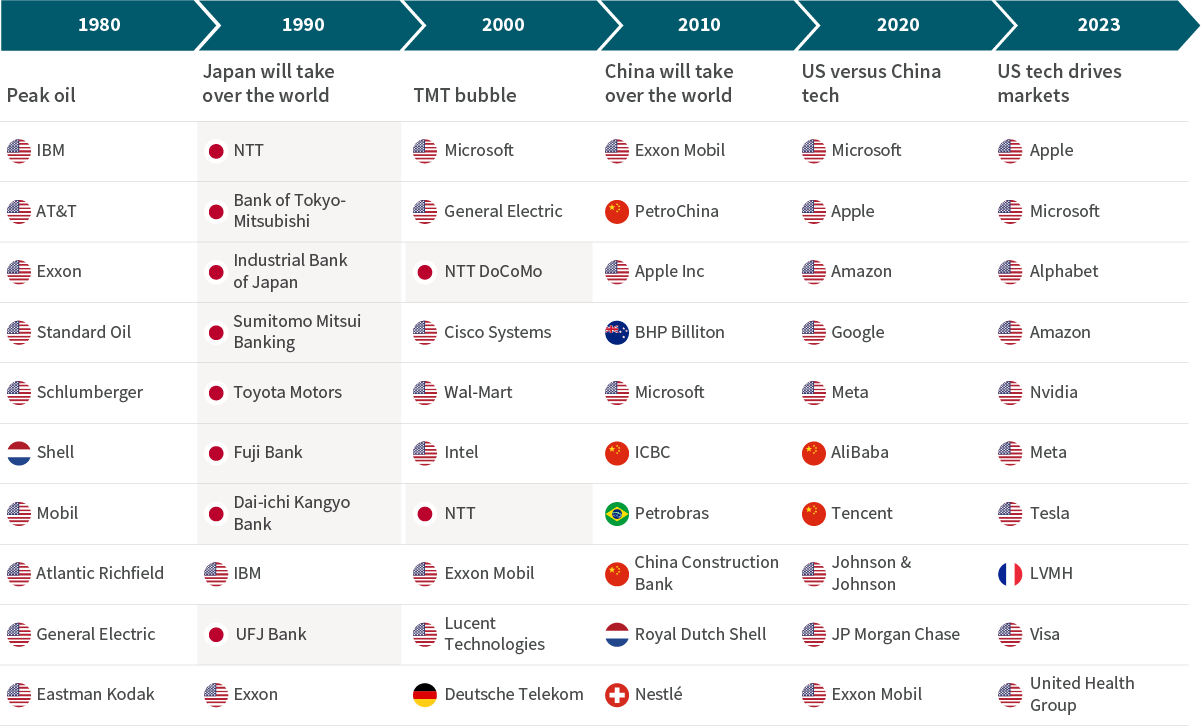

The effects of the lost decades can be seen in Japanese companies’ decline on the world stage. Whereas in 1990, eight of the ten biggest companies in the world by market cap were Japanese, there were only two by 2000, and for the last couple of decades, none have made the list (see Figure 1).

Figure 1: Ten largest market capitalisations globally, 1980-2023

Note: Berkshire and Aramco have been excluded.

Source: Aviva Investors, February 2024. Data sources: pre-2023 – Macrobond, as of July 31, 2020; 2023 – Statista, as of August 30, 2023.

Rising sums

But now the story looks to be changing. Until recently, investors both domestic and international have not had much incentive to invest in Japanese equities. Yet the country’s economy and stock market have been shocked into better shape over the last two years, and Japanese equities are now at their highest level in 34 years (see Figure 2).

Two key factors have reawakened the sleeping giant that was Japan’s economy: the move from a deflationary to an inflationary environment, and a swathe of crucial governance reforms.

Figure 2: TOPIX index, 1990-2024

Source: Aviva Investors, Bloomberg. Data as of February 26, 2024.

The result is investors are now finally getting more of a return for the money they are putting in, especially when other initiatives are also encouraging Japanese citizens to invest more of their capital domestically. But while inflation is providing a sugar rush for Japanese stocks, structural reforms will be key to realising their long-term potential.

Japan’s inflation rate increased after COVID-19 and Russia’s invasion of Ukraine

As with most other major economies, Japan’s inflation rate increased after the world’s emergence from COVID-19 lockdowns and the global supply-chain pressures that followed Russia’s invasion of Ukraine. Inflation reached 4.3 per cent in January 2023; it has fallen slightly since then but remained at 2.6 per cent in December – above the BoJ’s two per cent inflation target.4

Overall, the economy is looking healthier too, in spite of the recent quarterly contraction. Taking a longer-term perspective, earnings growth is reasonable. Valuations of world-class Japanese companies are relatively cheap (see Figure 3), so we are looking at earnings for evidence of the positive effects of inflation for companies, particularly on top-line growth and margin expansion. We are looking for increasing costs being passed through to consumers and additional value thus being generated, which should lead to higher corporate earnings and wages. While evidence for this will take time to come through, earnings per share (EPS) and sales growth metrics are positive and overall earnings estimates for Japan are being revised up, which is encouraging.5

Figure 3: Price to book ratio, TOPIX, Euro Stoxx 50, S&P 500

Note: S&P 500 composite is DS calculated.

Source: Aviva Investors, Reuters. Data as of February 26, 2024.

Governance reforms: From sugar rush to healthy living

What gives us confidence these positive trends will be sustained is the fresh momentum on corporate governance reform.

For a long time, Japan’s listed companies operated with little consideration for their shareholders, resulting in poor capital allocation, inefficiency and low margins relative to the rest of the world. In response, the Tokyo Stock Exchange (TSE), Ministry of Economy, Trade and Industry and Financial Services Agency jointly instigated a range of measures to improve the competitiveness and attractiveness of Japanese companies. As part of a broader economic programme to promote growth and address low corporate valuations, Japan is undergoing a multi-year period of corporate governance reform.

The Stewardship Code puts the onus on institutional investors to push investee companies to run as efficiently as possible

The Abe administration published a Stewardship Code in 2014, which it continues to improve. This code puts the onus on institutional investors to push investee companies, through voting and engagement, to run as efficiently as possible. That means a simplification of company structures, more independent directors, clarity around strategy and linking remuneration to performance.

Japan’s Corporate Governance Code was first introduced in 2015, complementing the Stewardship Code by calling on companies themselves to improve their governance standards. In its 2021 update, it emphasised improving board independence and diversity, workforce diversity, executive performance-linked remuneration practices and the consideration of sustainability challenges.

Additional reforms have been enacted to enable shareholders to challenge companies. They include reducing “cross-shareholdings”, reducing barriers to takeovers and reviving an environment for investors to collaboratively engage with firms.

Cross-shareholdings, a longstanding practice whereby companies hold shares in other firms with which they do business, have traditionally insulated management teams from challenges on the part of activist shareholders and locked up capital that might have been productively invested. The drive to reduce them is a key change brought by the corporate governance reforms.

All these measures combined could enable more growth and innovation, promote greater external investment and even encourage more M&A activity. Consolidation could further reduce inefficiencies. For example, there are several large auto manufacturers in Japan, which could arguably be brought down to a smaller number of larger, more-globally competitive firms.

Japanese listed companies have a strong incentive to be added to the Prime index as a sign of prestige

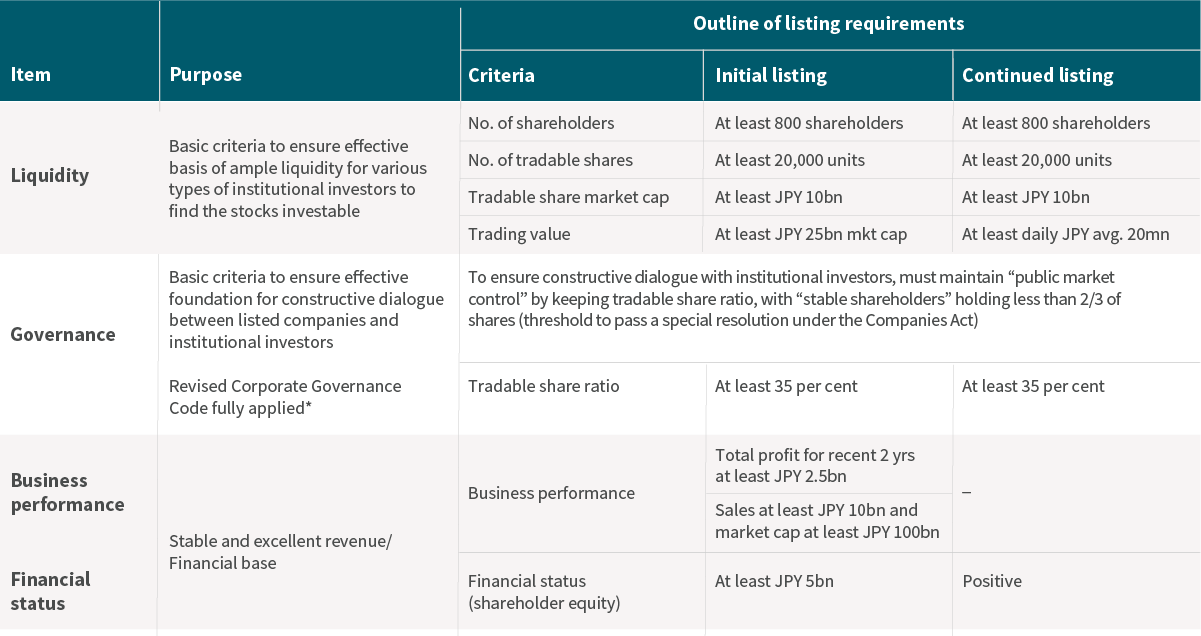

In 2023, the TSE launched a new index called Prime, which favours higher returns on equity and shareholder engagement (see Figure 4). The objective is to create a market that more closely resembles other developed markets, with better management of companies (see Engaging on governance). Japanese listed companies have a strong incentive to be added to the Prime index as a sign of prestige, pushing them to improve. As a result, since the creation of the index, the number of Japanese companies trading below book value has begun to drop. It is work in progress, but early results show there is more value to unlock. Over the long term, this and other reforms should help close Japanese stocks’ valuation gap with the rest of the world (see Figure 3).

Finally, an associated objective of the reforms is to ensure financial assets deliver returns to households, aiming to make the TOPIX equity index more investible for retail customers. Japan’s version of the ISA – called the NISA – has also evolved to encourage more capital flows into equities. The government is aiming to increase the proportion of equities in household assets from its current level of ten per cent to 20 per cent, to bring it in line with Europe and the US, which should support stock prices.

Figure 4: Listing criteria for the Prime market

Note: *Including principles requiring a higher level of governance applied to Prime-listed companies.

Source: Tokyo Stock Exchange. Data as of February 16, 2024.

Investment implications

Historically, there has been an inverse relationship between the TOPIX and the Japanese yen; when the yen has fallen, the TOPIX has done well because a weaker yen helped Japanese exports – and vice-versa. Since the pandemic, the overseas sales ratio for the TOPIX has risen sharply, to over 40 per cent excluding financials, which register sales slightly differently.6

The BoJ has said it would closely coordinate with the government in monitoring the Japanese yen and its impact on the economy

As a result, the currency is garnering interest from the BoJ, which has said it would closely coordinate with the government in monitoring the yen and its impact on the economy. The BoJ hasn’t stated it is targeting a specific currency level, but it wants to ensure exchange rates reflect economic fundamentals and move in a stable manner. As it has intervened in the past, it could well do so again.

As for the future path of base rates, rate rises look to be a case of when, rather than if, in spite of the disappointing quarterly economic data published in February. The BoJ recently said the likelihood of Japan sustainably achieving its two per cent inflation target is gradually rising and that it is increasingly confident conditions for phasing out its stimulus-like yield-curve-control (YCC) policy are falling into place.7 Lower inflation in the service sector was drawing slightly more concern, but the prospect of higher wages is gradually affecting sales prices, feeding through to an increase in service prices – the kind of virtuous cycle Japanese policymakers have long been striving for.

Figure 5: Japan’s perceived inflation outlook, one and three years ahead (per cent)

Source: Aviva Investors, Business surveys, Bank of Japan, TANKAN Inflation outlook, All Enterprises, All Industries. Data as of January 2024.

If Japanese interest rates rise, the yen could also climb.8 While a moderately stronger yen versus the US dollar could bring challenges for companies, it may not necessarily be a negative for Japanese equities. Japanese companies have expanded their overseas production and shifted to higher-quality exports to avoid competing on price with manufacturers elsewhere in Asia. This has caused both their share prices and earnings to become less sensitive to currency moves. As shown in Figure 6, the correlation between the yen and both earnings per share (EPS) and stock prices has weakened since 2016.

Given the current levels of the yen, we are primarily concerned about the asymmetry. We are therefore overweight both the yen and the TOPIX, supported by inflation and reforms. We are, however, underweight Japanese government bonds, due to our expectations of rate rises and a consequent fall in these bonds’ prices.

Figure 6: TOPIX, TOPIX EPS and USD/JPY exchange rate

Source: Aviva Investors, LSEG Datastream. Data as of February 2024.

This isn’t the first time we have seen attempts at structural reforms in Japan, but previous efforts did not gain sufficient momentum to launch a virtuous cycle. This time, however, the reforms are focused on building robustness; but, more importantly, Japan is moving out of deflation. These factors in combination mean reform is likely to be a lot more effective and so far, we have seen a real consensus building, helped by a more engaged TSE.

If inflation is sustained, this will help buoy corporate earnings and be an accelerant for corporate governance reforms which will be key to unlock the country’s long-term value potential.9 They should also encourage investment for growth by Japanese companies, which could help address some of the barriers to broader environmental, social and governance (ESG) challenges such as climate change, by spurring innovation.