Amid all the excitement about renewable energy and the emergence of other new technologies to help countries tackle climate change, all too often two important challenges are being overlooked.

The energy transition aims for a sustainable economy based on renewable, or low-carbon power. But making the necessary wind turbines, solar panels, electric car batteries, and other green products requires vast amounts of resources. Extracting them creates emissions of their own, as well as causing environmental degradation and, in many instances, social problems.

Take electric vehicles. While they may cause no emissions when being driven, the same cannot be said for the manufacturing process. As the technology begins to go mainstream, more ‘circular’ solutions will be needed. That is especially true of batteries, with the mining of materials such as nickel, cobalt and lithium threatening the environment.

Equally problematic is the challenge of recycling, storing and disposing of the waste created when products come to the end of their useful life. Even if tackling the waste generated by wind and solar is straightforward compared with nuclear, another form of low-carbon energy, it is an issue companies and investors alike have all too often overlooked.

Capacity surge

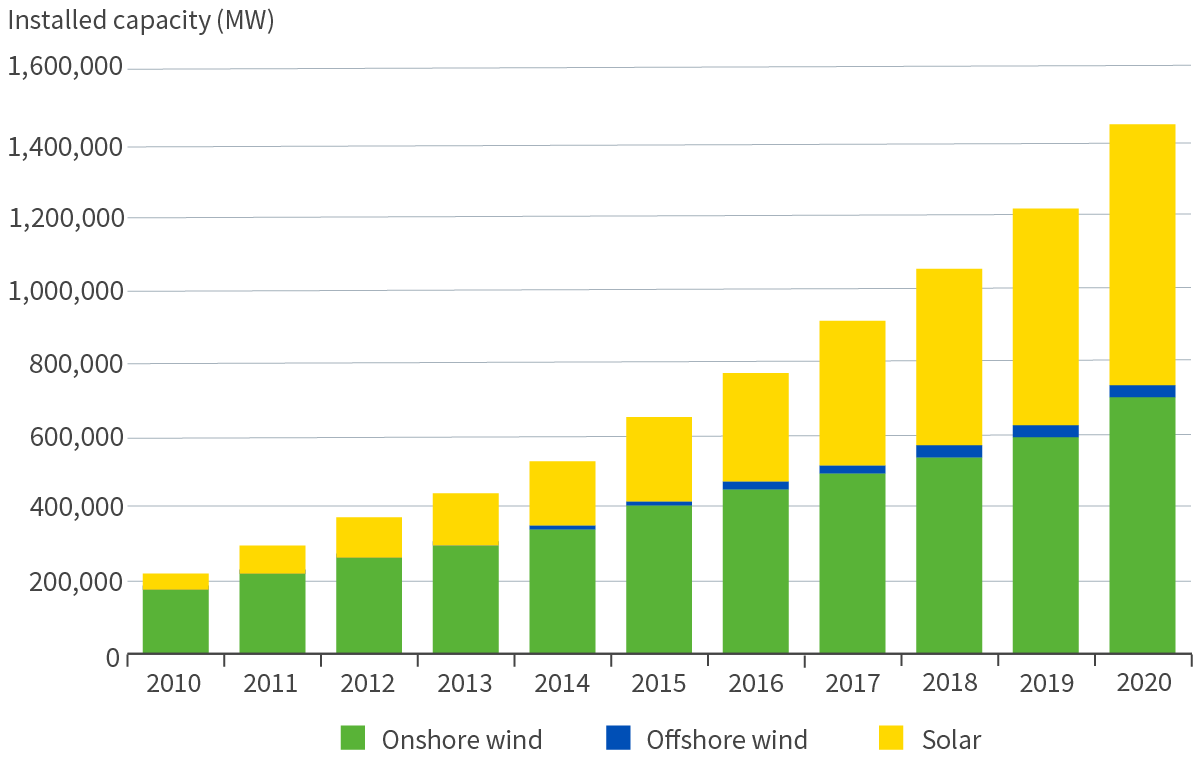

According to the International Renewable Energy Agency (IRENA), despite the economic disruption caused by the COVID-19 pandemic, the world added more than 260 gigawatts of renewable energy capacity in 2020, smashing previous records. That took global installed wind and solar capacity to more than 1.4 million megawatts, a near sevenfold increase in the space of a decade.1

Figure 1: Trends in renewable energy2

Source: International Renewable Energy Agency, 2021

IRENA reckons renewable energy capacity needs to grow eight times faster than the current rate to keep pace with rising demand for electricity and at the same time limit global warming. It believes $131 trillion of investment in renewables could be needed by 2050.3

Since most renewable installations are relatively new, waste has been largely limited to outdated or damaged products. However, with some older wind and solar farms starting to reach the end of their useful life, questions are being asked about what will happen to the waste, especially since the amount currently being generated will be dwarfed by what lies ahead.

“Industry has generally turned a blind eye to this area, but with net-zero commitments, it will be challenging not to start thinking about lifecycle emissions. This will naturally shine a light on disposal and dismantling issues from renewables,” says Ed Dixon, head of ESG, real assets at Aviva Investors.

Across the world, thousands of wind turbines are set to be dismantled over the next few years. While most components, including steel, copper wire and electronics, can be recycled, the blades have bedevilled energy developers and waste management experts. Made of a tough but pliable mix of resin and fibreglass, they are difficult to crush or recycle. They are also massive – some are longer than a Boeing 747 wing – and strong, built to withstand hurricane-force winds.

In most countries, blades are usually cut down and buried in landfill sites. The problem is that in the US alone around 8,000 blades are due to be removed in each of the next four years. According to one report, the country will have more than 720,000 tonnes of blades to dispose of over the next 20 years.4

The issues associated with dumping turbine blades in landfill sites may seem trivial compared with those associated with burning fossil fuels and dealing with nuclear waste. Nevertheless, the public image of an industry keen to promote its environmental credentials threatens to be tarnished, especially if the mass disposal of blades overwhelms existing landfill capacities as some fear. The race is on to find a better solution.

Circular economy

According to the European Union's 2020 Circular Economy Action Plan, adopted in March 2020, developing a truly circular economy will be "one of the main blocks" of the European Green Deal and a prerequisite for achieving climate-neutrality. Already, four EU countries have banned composites, including wind turbine blades, from going into landfill, while France and Germany are implementing or considering specific legislation on turbines and blade circularity.

Four EU countries have already banned composites from going into landfill

While some blades are burned in power plants, wind developers recognise this is a sub-optimal solution and are exploring ways to recover materials to safeguard their green reputations. In January, a consortium of ten companies launched a project seeking to commercialise recycling techniques for up to 95 per cent of each blade.5

One member of the consortium, GE Renewable Energy, recently announced a multi-year agreement with Veolia North America for a blade-recycling programme. The scheme involves shredding blades at Veolia’s Missouri facility, then using the output as a raw material for cement. Better still, according to a company news release, this process could reduce net emissions from cement production by a quarter.6

German company Neocomp has a similar solution, using flakes of composite material for the production of concrete, while another US company, Global Fiberglass Solutions, grinds blades up into chocolate chip-sized pellets for use in decking materials, pallets and piping. Its aim is to create a “circular, zero-waste solution to bypass land-filling of fibreglass waste and to reduce the world’s carbon footprint”.

Danish renewable power group Orsted says since recycling technologies will differ from market to market, it will assess the best locally available solutions on factors such as price, capacity, and environmental footprint.

Recycling is unlikely to cost any more than landfilling

“With a range of solutions likely to be on the market by 2025, recycling is unlikely to cost any more than landfilling,” says the company’s head of sustainability, Filip Engel.

However, others remain to be convinced new technologies can be successfully commercialised, or whether facilities can keep pace with demand. WindEurope, a trade association representing 400 companies across Europe’s wind power industry, says while an increasing number of companies offer various recycling technologies, “these solutions are not yet mature enough, widely available at industrial scale and/or cost competitive”.

Mark Nelson of US firm Radiant Energy Fund, which advises non-profit organisations and industry bodies on energy policy, says recycling technologies may “take some of the sting” out of the issue of wind turbine waste, but there is no escaping the fact there will be a public cost associated with the growing need to deal with materials from damaged or retired wind turbines.

“Recycling is not going to completely make up for the fact that suddenly there’s a thing called wind turbine waste, where in the public mind there was no such thing ten years ago,” he says.

Solar’s record growth

Although the world may have been building wind farms at a rapid rate, the sector’s growth pales in comparison with that of solar energy. According to the International Energy Agency, solar output grew more than any other source of energy for the first time in history in 2016.7

Despite snags in supply chains as a result of the pandemic, a record 138.2 gigawatts (GW) of solar capacity was added in 2020, according to trade association Solar Power Europe, an 18 per cent increase on 2019. The top five markets were China, US, Vietnam, Japan and Australia, which added new capacity of 48.2, 19.2, 11.6, 8.2 and 5.1 GW respectively.8

The sector’s exponential growth has been driven by a dramatic fall in the cost of producing solar panels. Between 1976 and 2019, the price of a photovoltaic module collapsed from $106 to $0.38 per watt.

Figure 2: The price of solar module declined by 99.6% since 19769

Note: The prices are adjusted for inflation and presented in 2019 US$.

Source: Our World in Data, 2020

Solar’s growth looks set to continue for two reasons. First, the cost of panels is likely to drop further. At the same time, new technologies mean they will continue to get more efficient – conversion efficiency is estimated to grow at a rate of around 0.5 per cent a year.

Solar Power Europe believes global installed capacity will more than double by the end of 2025, and under optimal conditions could be three times larger than today. Some countries look set for even quicker growth. Wood Mackenzie, an energy research and consultancy group, estimates the size of the US solar fleet will more than quadruple by 2030.10

Figure 3: Solar catching alight11,12

Source: IEA, June 2020 and SolarPower Europe, July 2021

However, while the rapid growth in solar power generation is welcome from the perspective of tackling climate change, it comes with an important caveat. In an industry where circular solutions such as recycling remain woefully inadequate, the sheer volume of discarded panels could become a key issue.

As Figure 4 shows, according to the US Department of Energy, solar uses more raw materials per unit of electricity generated than all other energy sources, in most cases by a significant margin. A report published by the International Energy Agency Photovoltaic Power Systems Programme and IRENA in 2016 said up to eight million tonnes of waste were expected to have accumulated by 2030, rising to as much as 78 million tonnes by 2050.13 Some believe these forecasts are conservative since they assume households hold on to panels for the entirety of their lifespan, which IRENA estimates at roughly 30 years.

Figure 4: Materials usage by energy type14

Source: Quadrennial Technology Review: An Assessment of Energy Technologies and Research Opportunities, Table 10.4, page 390. US Department of Energy.

Three business school professors cast doubt on these forecasts in a recent article in the Harvard Business Review. They said three variables are crucial in determining replacement decisions: the installation price, the going rate for selling solar energy back to the grid, and the efficiency of panels.15

Consumers may decide to upgrade far faster than IRENA expects

Should prices decline and efficiency improve as expected, consumers may decide to upgrade far faster than IRENA expects, regardless of whether their existing panels have reached the end of their useful life. Moreover, “with commercial and industrial panels added to the picture, the scale of replacements could be much, much larger”, the authors wrote.

As studies suggest solar panels retain upwards of 80 per cent of their original operating efficiency after 25 years of use – one study claims as much as 94 per cent – a solution that has been touted is to ship second-hand panels to poorer nations. After all, the World Bank reckons in 2019 there were 759 million people in sub-Saharan Africa and Asia without access to electricity and a further billion people with an unreliable grid.16

Since many of these countries have plenty of sunshine, this potentially offers them a cost-effective way of keeping emissions down. BloombergQuint in August reported one recent deal saw 25 megawatts-worth of panels (weighing as much as 2,000 tonnes) shipped to Afghanistan from the US.17

The World Bank says more than a billion people gained access to electricity between 2010 and 2019. While some of that gap was closed by new power lines and other transmission facilities, most of it was achieved by installing small solar systems designed to power a village, farm or even a single home. As of last year, 420 million people got their electricity from off-grid solar systems. According to the World Bank, that number could nearly double by 2030.

Orphan waste?

However, while this may on the surface appear a win-win solution, not everyone agrees. Every solar panel eventually reaches the end of its useful life. By shipping panels to developing countries, richer nations are arguably shifting the burden of dealing with waste in a responsible fashion to other countries less able to meet the challenge.

The issue of solar waste is not only one of volume. Solar panels contain toxic metals like lead, which can damage the nervous system, as well as cadmium, a known carcinogen. Both are known to leach out of existing e-waste dumps into drinking water supplies. According to Michael Schellenberger, author of the 2020 book Apocalyse Never and long-time advocate of nuclear energy, solar panels create 300 times more toxic waste per unit of energy than nuclear power plants, by volume.

Solar panels create 300 times more toxic waste per unit of energy than nuclear power plants, by volume

In any case, given the scale of the problem, shipping panels to developing countries offers no more than a partial solution. The widespread adoption of recycling technologies will still be needed. There are two main types of solar panels – silicon based and thin-film based. While both can be recycled, different industrial processes are needed.

The process of recycling the former begins with separating the aluminium and glass parts. Almost all of the glass can be reused, while all external metal parts are used for re-moulding cell frames. The remainder of the materials are heated to 500°C to separate the constituent parts, with up to 80 per cent capable of being re-used.

As for thin-film based panels, they are shredded before being separated using a rotating screw. On average, 95 per cent of the semiconductor material is reused, while as much as 90 per cent of the glass elements are saved for re-manufacturing.

The (current) problem is that while panels contain small amounts of valuable materials such as silver and copper, it costs more to extract these elements from the panels than to dump the used panels in landfill and mine fresh raw materials from the ground.

Take it back

In an effort to tackle the problem, Europe has since 2012 required solar panel producers to take back and dispose of modules sold in the bloc in a more environmentally sound fashion. The EU’s Waste Electrical and Electronic Equipment directive mandates member states to adopt waste-management programmes. Under the legislation, which was updated in 2018, producers are responsible for recovering up to 85 per cent of the waste generated and reusing or recycling 80 per cent of the recovered amount.

Europe has required solar panel producers to take back and dispose of modules in a more environmentally friendly fashion

The EU’s aim is twofold: to encourage the industry to develop products that are easier to recycle and use fewer raw materials; and secondly, to get producers to factor in the cost of the collection and end-of-life treatment of their products into the cost paid by consumers.

However, some see flaws in the legislation, arguing that while up-front recycling fees make sense in theory, they do not always work well since they are complicated to implement. The danger is that less scrupulous operators will look to game the system and will not be in business by the time their panels are being dismantled.

A second criticism of the directive is that it is all too easy to fulfil by recovering just the glass and the aluminium – the main raw materials – and that regulators need to target the recycling of materials, such as silicon, which have a much higher carbon footprint.

That said, the situation is bleaker elsewhere. Outside of Europe, the lack of regulation and unfavourable economics means most waste ends up being dumped alongside the larger global stream of electronic waste.

While many are confident photovoltaic recycling technology can and will be improved, at present there is insufficient economic incentive to invest in recycling capacity. Until that changes, some other solution needs to be found: leave the panels where they are; dismantle them and put them in storage until recycling capacity is available; put them in landfills; or ship them to developing countries. None are attractive economically, environmentally or socially.

The US government-funded National Renewable Energy Laboratory concurs. “There is little incentive for private industry to invest in PV recycling, repair, or reuse due to current market conditions and regulatory barriers,” it says.18

It is calling for government support into R&D and the creation of other policies to spur private investment into designing PV modules that are more easily repaired, reused, or recycled.

The Association for Renewable Energy and Clean Technology, a UK trade body, agrees. It says while legislation exists which ensures that solar waste is not a harm to the environment, “this does not guarantee it will be used for the most environmentally conscious purpose”.

Policy measures to increase the UK’s capacity for managing solar components recycling would be beneficial

“Policy measures to increase the UK’s capacity for managing the recycling of old solar components, and incentives that encourage the appropriate disposal of old solar units, would be beneficial,” the UK group’s chief executive Dr Nina Skoprupska says.

She believes if the recycling/upcycling supply chain were to become more firmly established, it is feasible that making reconditioned solar panels could become comparable in cost to making them from scratch.

However, Nelson, who in 2017 became one of the first people to highlight the issue of waste in the solar energy industry, disagrees. He says even if the cost of recycling is not especially high for utility-scale solar, as with wind turbine blades, sending them to landfill will remain cheaper, even when more effective recycling techniques emerge.

“The problem is that while recycling metals is profitable, very little else is. We may be dismayed by the toxicity and lack of usability of recovered materials, or pleasantly surprised by their value. But while solar may be easier to recycle than plastic, which is little more than a marketing scam, it will never be profitable, even at scale,” he says.

That said, few believe the extra cost of dealing with the waste in a more environmentally friendly fashion will seriously undermine the favourable economics of solar energy.

Nimbyism and nuclear

Nowhere is the waste challenge more evident than in the nuclear energy industry. Providing about ten per cent of the world’s electricity from around 445 reactors, it is the second largest source of low-carbon power.

The world has yet to build a single permanent disposal facility for commercial nuclear plants

However, more than sixty years after the first commercial nuclear plants began operating, the world has yet to build a single permanent disposal facility. The International Atomic Energy Agency said in 2018 that, as of 2013, the global civil nuclear industry had generated 370,000 tonnes of high-level radioactive waste in the form of spent fuel. With just under a third estimated to have been reprocessed for re-use in reactors, the remaining 250,000 tonnes – with an equivalent volume of approximately 22,000m3 – is being held in temporary storage facilities.19

In May, Finnish waste management company Posiva Oy, announced the start of excavation on a deep geologic nuclear waste repository. Operation is expected to begin in 2023, with the project estimated to cost about €2.6 billion ($3.04 billion). About a dozen other countries are planning deep geological repositories for their nuclear waste. But the discussions have been bedevilled by political opposition, with few wanting long-term depositories built on their doorstep.

In October 2020, the company responsible for disposing all of Sweden’s nuclear waste said it had already won approvals from all necessary courts, authorities and even the municipality where it wants to build the site – but not the Swedish government.

The Scandinavian country is running out of space to store the waste produced by its six reactors, which supply about a third of the nation’s power. Without a decision soon, nuclear operators including Vattenfall AB say they will have to start halting production in just three years. That would trigger a national power crisis and put Sweden’s net-zero target at risk.

In the US, a long-standing proposal to build a repository beneath Yucca Mountain in Nevada was approved as far back as 1987 by President Ronald Reagan. The site was supposed to begin accepting spent fuel in 1998. However, the legislation, which became known as the “Screw Nevada Bill”, faced stiff opposition from the public, a native American tribe and state politicians.

Having drifted in and out of favour with changes in the political landscape, it appears the plans have finally been killed off as President Joe Biden goes back to the drawing board. In June, US Energy Secretary Jennifer Granholm said while it was a priority to fund and find a long-term disposal solution to nuclear waste, “it’s not going to be Yucca Mountain”.20

Waste accumulates mainly where it is generated – at the power plants and processing facilities

For now, waste accumulates mainly where it is generated – at the power plants and processing facilities. Some of it has been sitting in interim storage for decades. According to one report, with the cost of that effort having already grown to $7.5 billion by 2019, the government expected the eventual cost would rise to $35.5 billion. Since the longer it dithers, the higher the cost, others within the industry reckon the government will end up with a significantly higher bill. 21

While it remains to be seen how important a role it will play in helping the world combat climate change, the nuclear industry’s inability to find a permanent home for its waste has been a long-standing impediment to more widespread adoption of the technology.

Darryl Murphy, managing director of infrastructure at Aviva Investors, says the nuclear waste problem provides a salutary lesson to investors in renewables why they need to confront the issue head on, even if the problem of dealing with waste from wind and solar pale in comparison.

“Given the need to look at the lifecycle of assets when assessing their carbon credentials, investors are going to have to start to care about the decommissioning stage, which I don’t believe they have done adequately to date,” he says.

Companies providing support services or new technologies to the green energy sector are well placed to grow rapidly over time

Murphy believes this means companies providing support services or new technologies to the green energy sector are well placed to grow rapidly over time. That should in turn provide attractive investment opportunities once the regulatory landscape becomes clearer.

In July, Redwood Materials raised more than $700 million from investors to expand operations, valuing it at $3.7 billion and making it worth more than any other US battery recycling group. The company expects to process 20,000 tonnes of scrap and has already recovered enough material to build 45,000 electric vehicle battery packs.22

However, Aviva Investors’ global equity fund manager Will Malcolm says even if the extra costs do not badly damage the case for renewables, this could present challenges to the energy providers themselves, which for the past two decades have largely focused on lowering costs.

Government action needed

“It is becoming increasingly evident all stakeholders involved in the wind and solar industries – governments, the companies themselves and investors – need to ensure the potential problems of tomorrow prove manageable,” he says. The faster the renewable energy industry gets to grips with its waste issue by creating a more circular economy, the better for all concerned.

You need to start by admitting it comes with a cost and then work out who pays

As for Nelson, he believes it would be unwise to rely on the generosity and good stewardship of renewable energy investors and vendors or on the value of the bulk of the solar and wind materials themselves. Rather, governments need to start acting quickly if the necessary investment in wind and solar waste handlers is to happen before it is too late.

While there’s no denying the critical contribution of renewables to combatting climate change, for waste to be dealt with in an environmentally friendly way, people need to have confidence governments are taking the issue seriously by mandating recycling.

“You need to start by admitting it comes with a cost and then work out who pays. The sooner governments make up their mind the better,” Nelson says.