As many central banks begin cutting interest rates, short-term bond strategies can offer a complement to cash holdings. Alastair Sewell explains.

Read this article to understand:

- The importance of assessing cash exposures

- The key features of short-term bond strategies

- Why the Aviva Investors ReturnPlus strategy can offer a viable complement to cash

Investors hold cash or near-cash assets for many reasons. At a simple level cash is the lifeblood of any organisation. A certain amount is always needed or generated as a function of purchases and sales. With larger or more significant planned actions or events – think M&A, a major funding activity, a dividend payment – it may be desirable to build up a reserve of cash. At another level cash has a contingency role – a store of value against unknown events.

In short, cash has value. Unfortunately, a value that many investors do not realise. Unless properly allocated, cash returns can be poor. Overnight deposit rates at banks typically fall far short of the rates available in the interbank market. For those investors storing cash in bank deposits, they may be leaving income on the table. Conversely, those able to access the rates available in the interbank market, through tools such as money market funds (MMFs), may be able to access attractive rates.

When interest rates are low, income generated on cash will be low. When interest rates are higher, cash can offer the tantalising proposition of good levels of income combined with the key benefits cash brings: stability of value and accessibility. When interest rates change, many investors will assess the amount of cash they hold, how they hold it, and whether they should make any changes to their allocation.

In this article, we set out some of the investor considerations for stepping out of cash and the options available.

Assessing cash exposure

When reviewing cash allocations, it’s important first to review the advantages of holding cash and also to consider whether cash is allocated as efficiently as possible.

Liquidity and flexibility

Cash and near-cash assets offer unparalleled liquidity and flexibility. Cash allows for easy access to funds to meet short-term liabilities and unexpected expenses. In periods of market volatility, having liquid assets can provide a buffer and enable swift reallocation to capitalise on emerging opportunities or to rebalance portfolios.

It’s worth noting that a term or fixed cash deposit does not provide liquidity. While cash deposits of up to 90 days may be recognised as “cash” for accounting purposes, this cash will not be available till the end of the term. So while it is cash, it is not as liquid as cash in overnight deposits or MMFs offering same day dealing and settlement.

Capital preservation

One of the primary advantages of cash and near-cash investments is capital preservation. In an uncertain economic environment, the safety of principal becomes paramount. Cash held at banks is subject to credit risk on the bank (when not benefitting from government guarantee or similar mechanisms). MMFs, on the other hand, diversify risk across multiple counterparties.

Balance sheet and capital purposes

Cash also serves important purposes for many different entity types, beyond its core roles. For example:

- Corporations: Cash and cash equivalents are reported on balance sheets and are an important metric tracked by investors. Rating agencies will factor cash balances into their assessment methodologies. Maintaining certain levels of cash can be an important consideration for these third parties.

- Insurers: Insurance regulators are focused on liquidity risk, including for life insurers. In some jurisdictions regulator-defined liquidity waterfalls and stress tests aim to ensure insurers have sufficient liquidity to resist adverse market developments. Cash and near cash are high “value” assets in these frameworks.

- Pension funds: While cash outlays from schemes to members are predictable, where schemes use leveraged strategies, liquidity – and hence liquid assets including cash – become important considerations.

A source of yield

Cash can have a bad reputation. Many assume cash is particularly vulnerable to erosion of value through inflation. This is simply not true. A more accurate statement is that cash left on deposits at banks can be vulnerable to erosion of value through inflation.

Indeed, deposit rates offered by banks may well be below inflation, leading to “cash drag”.

On the other hand, central bank rates – and hence interbank rates – typically exceed inflation (see Figure 1). Therefore, if an investor can hold cash at or around these levels, they can preserve value in real terms. MMFs typically target interbank rates such as the US Federal Reserve’s Secured Overnight Financing Rate Data (SOFR) or the European Central Bank' euro short-term rate (€STR). The combination of potentially inflation-beating returns and low volatility can make MMFs an attractive allocation in general – particularly for cash – in a range of market scenarios.

Figure 1: Average cash returns, 1901-2022 (per cent)

Past performance is not a reliable indicator of future returns.

Source: Aviva Investors, Morningstar, DMS database. Data as of January 27, 2025.

However, the income MMFs can generate will vary, anchored in central bank rates. When rates are falling, near-cash options such as short-term bonds can serve as a useful complement to MMFs, potentially offering higher yields.

Short-term bond strategies: a viable complement

Some investors – such as those with strategic or longer-term cash balances, or indeed those seeking to increase the blended yield on their liquidity allocation – may benefit from diversifying their cash allocations into a wider range of options.

Enhanced yield potential

Short-term bond strategies can be an attractive complement to cash investments such as MMFs. These strategies will typically target higher yields than MMFs by investing in a wider range of securities than MMFs and at longer maturities. By extending the investment horizon slightly, these strategies can capture higher yields compared with cash and near-cash instruments, thereby enhancing overall portfolio returns.

Diversification benefits

Incorporating short-term bond strategies into a portfolio can provide diversification benefits. These strategies typically invest in a broad array of securities, including government bonds, corporate bonds, and asset-backed securities. This diversification helps spread risk and can contribute to more stable returns. A key difference with MMFs is bank exposure. Most MMFs have a high exposure to banks, whereas short-term bond strategies can diversify into other sectors and security types.

Selection considerations

One of the key considerations for investors considering an allocation to short-term bond strategies is their risk exposure. With a broader range of risk profiles compared with MMFs, there are additional factors for investors to consider.

- Interest rate risk exposure: Many short-term bond strategies will have interest rate risk exposure. Many of these strategies will hold fixed-rate bonds with maturities of three to five years. This will equate to a materially higher duration than MMFs. Some strategies within the category will hedge interest risk, either naturally through allocating primarily to floating rate instruments or by using plain vanilla derivative instruments, such as interest rate swaps, to hedge interest rate risk. Strategies with higher levels of interest rate duration will be more sensitive to interest rate movements.

- Spread risk exposure: These strategies will also be more sensitive to movements in credit spreads than MMFs. Conversely, they will be less sensitive to credit spread movements than intermediate-term credit strategies. Credit spread duration is a measure of how much prices moves in relation to movements in credit spreads, themselves reflecting relative risk of default. Short-term bond strategies will have a range of credit spread duration exposures, up to around five years. Lower average levels will typically mean less volatility.

- Credit risk exposure: Many MMFs limit their credit selections to issuers rated above a minimum threshold, e.g. ‘A’. Short-term bond strategies may have a wider risk appetite. Many, in fact are active investors in corporate credit. While this exposure can bring diversification and potentially higher yields, it does so at the expense of higher default risk. There is a large population of corporates rated BBB. Indeed, fallen angels are defined as formerly investment-grade entities (typically BBB range) which have been downgraded to speculative grade. Some short-term bond strategies will also include speculative grade allocations. Risks in speculative grade securities are elevated.

- Asset classes: Corporate exposure can be material in some short-term bond strategies. Others may take a more nuanced view and opt for other asset classes. Covered bonds, for example, are typically rated AAA and can generate higher yields than similarly rated instruments. Some high-quality securitisations can also generate additional returns per unit of risk. From an investor perspective it’s important to understand the risk exposures in the strategy in question.

Case study: Aviva Investors ReturnPlus strategy

The Aviva Investors ReturnPlus strategy exemplifies the potential benefits of short-term bond strategies. This strategy focuses on providing enhanced returns through a diversified portfolio of short-duration bonds, including government and corporate bonds.

Performance metrics

Historical performance data indicates that the Aviva Investors ReturnPlus strategy has consistently delivered higher yields than traditional cash and near-cash investments. The strategy’s risk-adjusted returns have also been favourable, making it an attractive option for institutional investors seeking to optimise their portfolios.

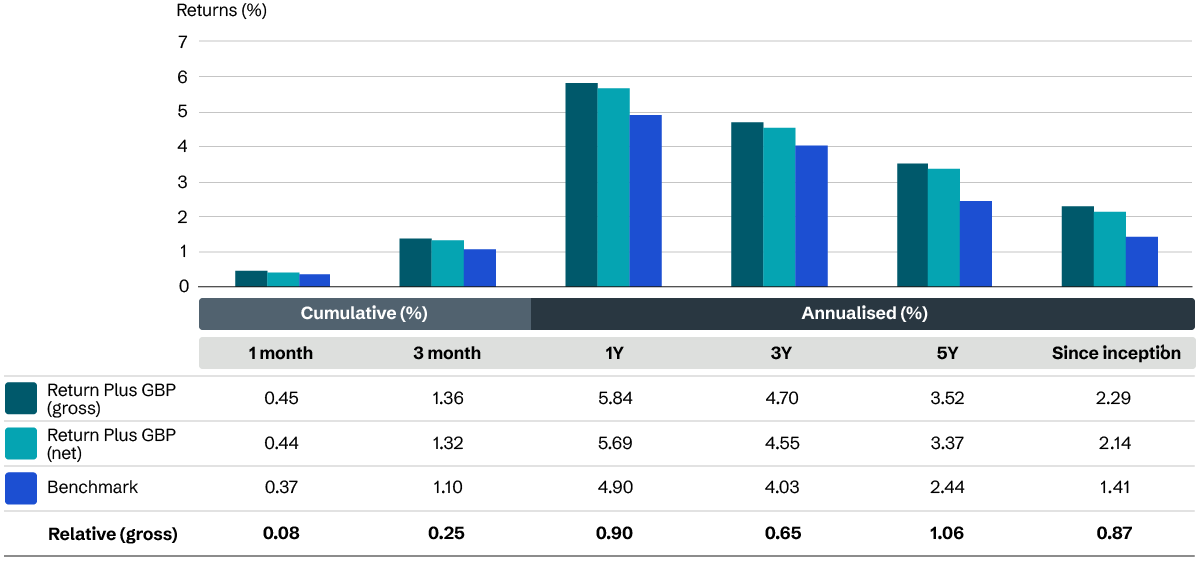

Figure 2: GBP: Investment Growth

Past performance is not a reliable indicator of future returns.

1. Inception date is 31 October 2014.

2. Performance net of indicative investment management fees of 15 bps. The effect of fees will reduce the overall return from the investor.

3. Benchmark is SONIA: Sterling Overnight Index Average.

Source: Morningstar as at 30th June 2025.

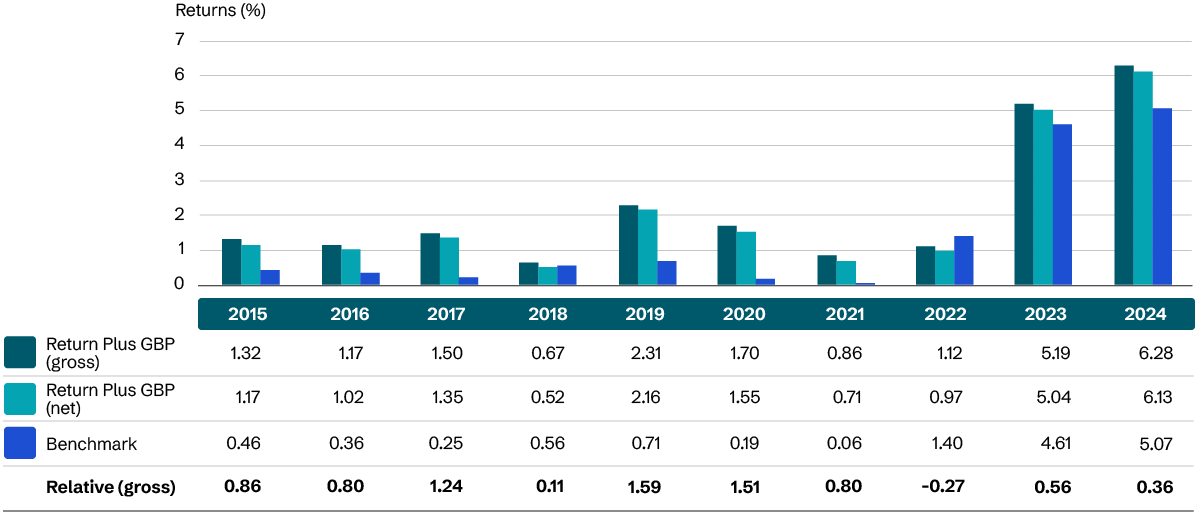

Figure 3: GBP Calendar year performance

Past performance is not a reliable indicator of future returns.

1. Inception date is 31 October 2014.

2. Performance is expressed gross of fees and fund expenses, in GBP. Performance net of indicative investment management fees of 15 bps. The effect of fees will reduce the overall return from the investor.

3. Benchmark is SONIA: Sterling Overnight Index Average. GIPS composite disclaimer can be found in the Appendix.

Source: Morningstar as at 30th June 2025.

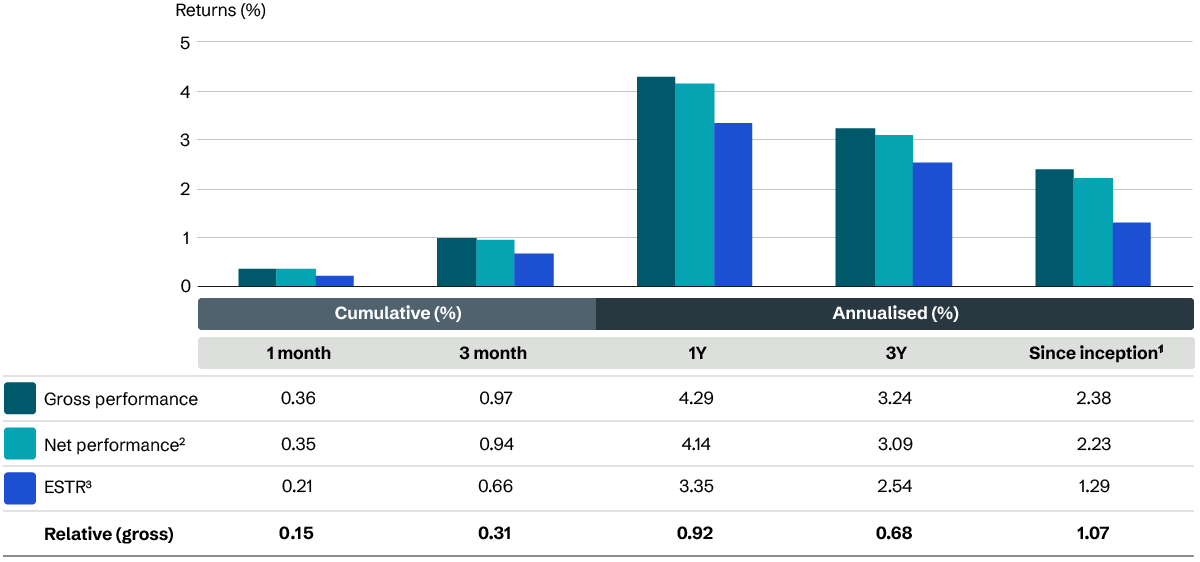

Figure 4: EUR: Investment Growth

Past performance is not a reliable indicator of future returns.

1. Inception date is 17 March 2020.

2. Performance net of indicative investment management fees of 15 bps. The effect of fees will reduce the overall return from the investor.

3. Benchmark is ESTR Euro Short Term Rate.

Source: Morningstar as at 30th June 2025.

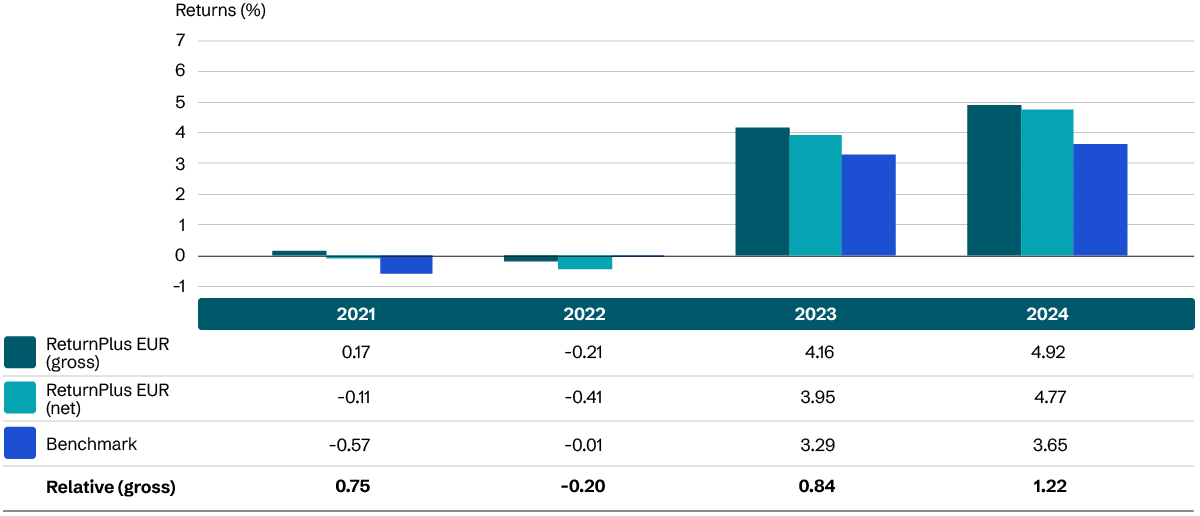

Figure 5: EUR: Investment Growth

Past performance is not a reliable indicator of future returns.

1. Inception date is 17 March 2020

2. Performance net of indicative investment management fees of 15 bps. The effect of fees will reduce the overall return from the investor.

3. Benchmark is ESTR Euro Short Term Rate

Source: Morningstar as at 30th June 2025.

Asset allocation

Unlike many short-term bond strategies, ReturnPlus has a minimum credit quality allocation of A, which is comparable with MMFs. This higher quality focus differentiates it from strategies with BBB or lower corporate credit exposures. ReturnPlus’s primary allocations are to covered bonds and sovereign, supranational and agency bonds, again, differentiating it from traditional corporate credit short-term bond strategies.

Furthermore, ReturnPlus hedges interest rate risk, resulting in an interest rate duration neutral exposure. This contributes to ReturnPlus’s lower volatility than many other short-term bond strategies.

Risk management

Risk management is a core component of the Aviva Investors ReturnPlus strategy. The strategy employs rigorous credit analysis and interest rate risk management techniques to ensure that the portfolio remains resilient in varying market conditions. This approach aligns well with the risk management objectives of insurers and pension funds.

Conclusion

The decision to step out of cash and into short-duration bonds involves careful consideration of multiple factors, including liquidity, risk, and regulatory requirements. Strategies like the Aviva Investors ReturnPlus strategy offer a viable alternative to enhance yields while maintaining a prudent risk profile. By strategically incorporating these strategies into their portfolios, institutional investors can achieve a balance between stability and growth in an ever-evolving financial landscape.