A set of megatrends is reshaping the world, creating new opportunities and risks for investments in private markets.

Read this article to understand:

- The long-term megatrends shaping the economies of tomorrow

- Why they are key to assessing private market investments

- How they can be incorporated into investment analysis and decisions

“Megatrends” are the significant long-term trends that shape our world – in technology, demographics, climate change and geopolitics – influencing multiple dimensions of our societies and economies.

They are inherently complex and interconnected and have far-reaching consequences. That makes their impact on long-term risks and asset performance difficult to quantify. Yet distilling these megatrends into a coherent and applicable framework is an essential task to better assess investment opportunities and risks.

They are particularly relevant in private markets, where investments are by nature longer term, less liquid and less transparent than in public markets. Private markets offer different risk and reward characteristics than public markets, something asset allocators are increasingly aware of (see Private Markets Study 2025).1

This has led us to articulate the forces at play into five overarching themes, providing broad enough coverage to capture the impacts of the megatrends but without overcomplicating the framework with excessive detail. Our goal was to create a clear and digestible approach to assessing the megatrends, to enable better, more informed investment decisions.

In our private markets platform, we have touchpoints across one of the largest franchises in Europe. That has enabled us to benefit from the investment desks’ operational leverage and intelligence to power our views. We then combined those insights with third-party and proprietary research to build our framework.

The five “TRENDs” we have identified are:

- Technology

- Resilience to climate and environmental risk

- Energy transition

- New global order, and

- Demographics

In this article, we explore each in turn and give some examples of investment implications for real estate, infrastructure, public sector and corporate investments, and the emerging assets that are venture and natural capital.

“T”: Technology will drive change

Technology will continue to be a key driver of innovation and economic growth. The trend is towards an increasingly digital economy driven by automation, systems and data. But it also encompasses a broader range of advancements in physical technologies that improve product or engineering efficiencies, like advanced materials, biotech and artificial intelligence (AI).

Dedicated infrastructure and services to enable further AI development and adoption will grow, presenting investment opportunities. In turn, the integration of AI into business models and the automation of manual processes will drive efficiency gains. However, there is a risk of disruption to business models and of possible job replacements.

Beyond AI and over the very long term, other trends are beginning to reshape economies.

In advanced manufacturing, innovations in manufacturing processes, including 3D printing and automation, are transforming production capabilities and efficiency.

Almost all economic sectors are increasingly adopting clean energy solutions – technologies focused on renewable energy sources, such as solar and wind power, as well as advancements in energy storage and grid management.

Materials science continues to develop new materials with unique properties, such as graphene and other nanomaterials, which have applications in various industries from electronics to healthcare.

The emerging field of quantum computing promises to revolutionise computing power, enabling the resolution of complex problems that classical computers can’t solve.

Advances in biotechnology – from gene editing to personalised medicine and synthetic biology – are opening new frontiers in healthcare and agriculture.

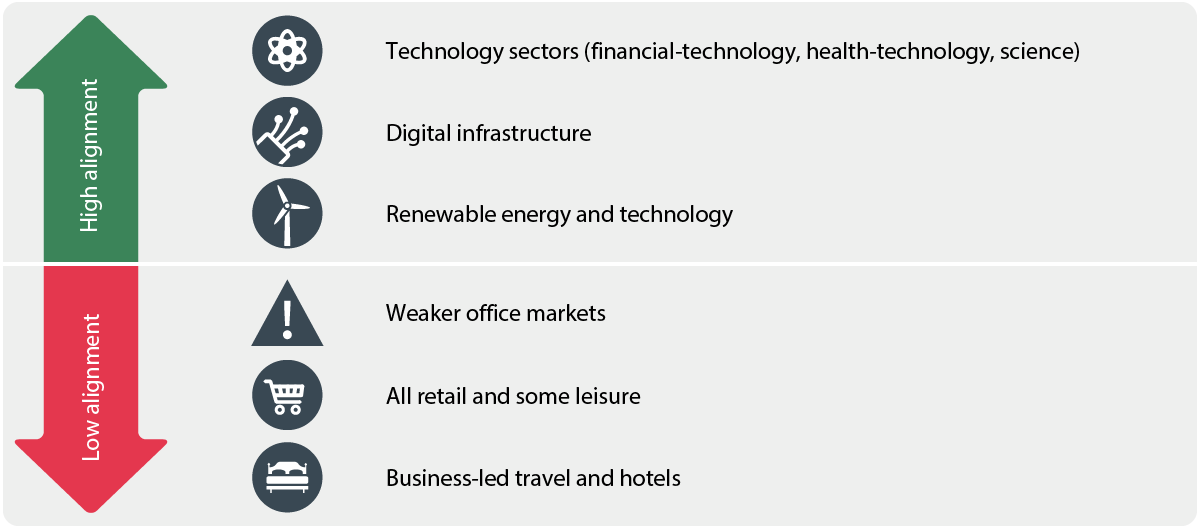

Figure 1: Sectors most and least aligned to technological changes

Source: Aviva Investors, as of May 2025.

“R”: Resilience to climate is a key risk factor

Understanding the speed and scale of physical climate risks driven by factors such as heatwaves, rising sea levels, temperature fluctuations, and collapse of biodiversity is hugely relevant to real assets. We therefore assess physical risk across private market sectors. This is especially relevant when there is direct exposure to an underlying real asset.

Physical risk is primarily driven by location and includes extreme weather events (heatwaves, rising sea levels, flood risk, temperature fluctuations) impacting land, real estate and infrastructure assets. The frequency of such events has increased over recent decades (see Figure 2). More resilient assets and locations should inherently be more protected from downside risks. Consequently, all else being equal, this resilience should be reflected in lower expected insurance premiums, thus reducing a potential drag on investment returns.

Figure 2: Global reported natural disasters by type, 1970 to 2024

Note: Data includes disasters recorded up to April 2024.

Source: Aviva Investors, Our World in Data, as of April 11, 2024.2

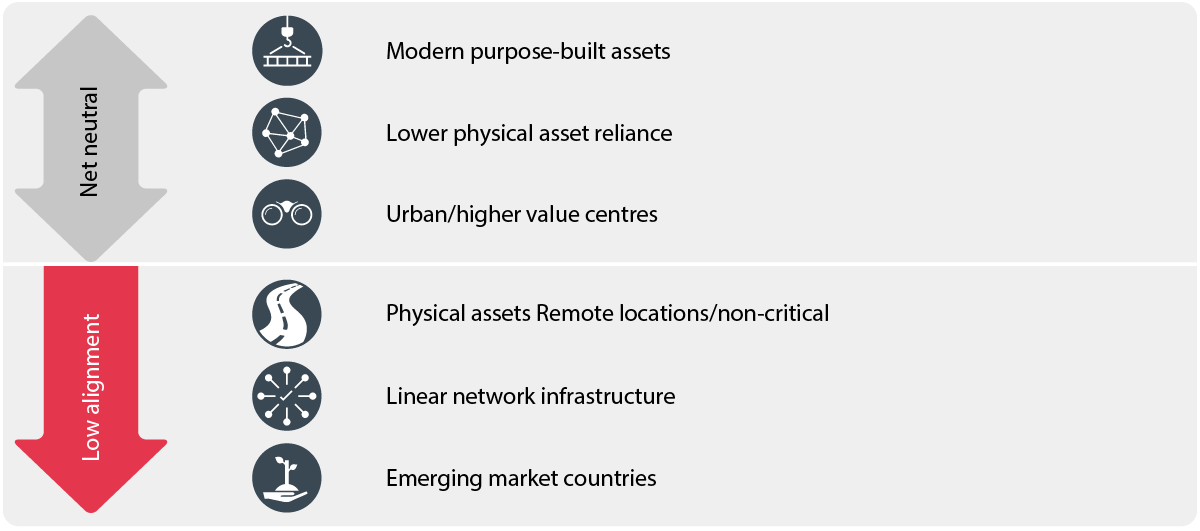

Meanwhile, climate adaptation involves protection against current and /or future climate impacts. Urban centres, economic hubs and critical infrastructure are more likely to benefit from potential adaptation strategies. However, there is a general lack of strategies to date to prevent against such long-term risks. And finally, linear network infrastructure such as cables, power lines, pipelines or railways that extend over long distances can be more vulnerable to disruption as damage to a single point could compromise the wider network.

Figure 3: Physical climate risk will have a lower impact on certain assets

Source: Aviva Investors, as of May 2025.

“E”: Energy transition

To lower global greenhouse-gas emissions and limit climate change, economies must transform – moving from using fossil fuels to zero-emissions electricity as their main source of energy. But the transition also involves improving the energy efficiency of buildings and industrial processes to reduce energy consumption and emissions. This is key to cut energy costs and improve economic competitiveness.

Adopting policies and regulations that support the energy transition is crucial, from subsidies for renewables to carbon pricing, emissions targets and EPC requirements. Policy change is extremely variable across countries. But when it comes, it could mean future costs to business models that are not aligned.

Investors need to understand market and technology risks, and the varying speed of policy adoption across regions, companies and assets

To navigate this transition, investors need to understand market and technology risks, and the varying speed of policy adoption across regions, companies and assets.

The most energy-intensive assets are data centres and, in real estate, hotels and shopping centres. However, the energy intensity and carbon emissions of buildings are closely correlated to their age and levels of activity. We are therefore more concerned about older stock, such as legacy social housing which can be of lower energy efficiency and faces higher retrofitting costs. Meanwhile, most logistics and manufacturing occupiers are yet to transition, and rely on carbon-intensive operations. This presents risks around regulatory non-compliance and rising energy costs, but also opportunities for long-term investors looking to unlock value through decarbonisation and asset repositioning.

In contrast, some of the most resilient areas include self-storage, prime office and new purpose-built single-family housing as they typically feature modern energy-efficient designs and lower operational emissions.

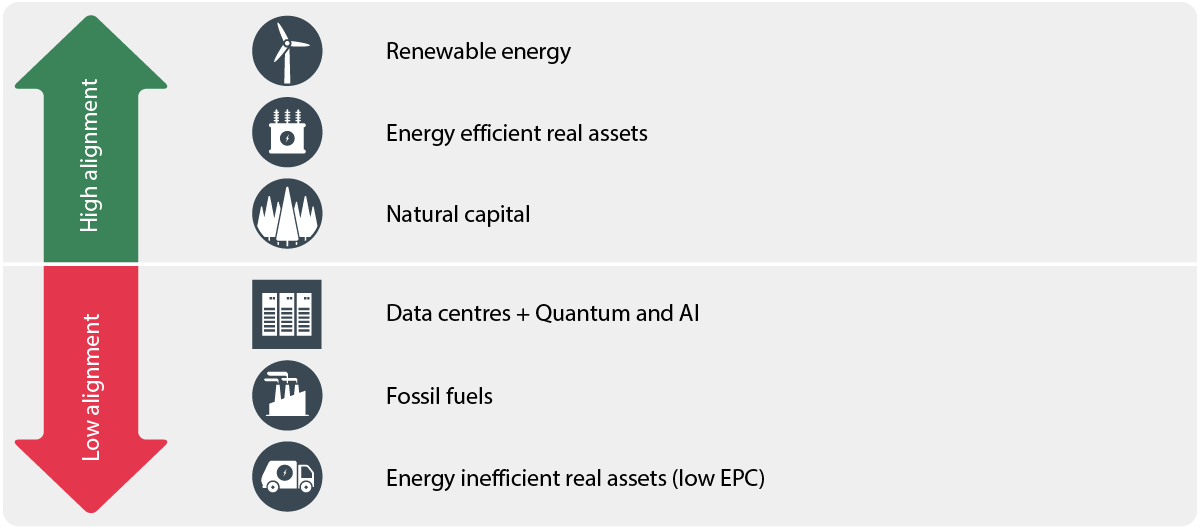

Figure 4: Sectors most and least aligned to the energy transition

Source: Aviva Investors, as of May 2025.

“N”: New global order

Geopolitical fault lines are being redrawn. This encompasses deglobalisation, but also other changes happening globally which impact private markets, from migration to mobility, conflict, and energy and data security.

After 80 years of increasing trade liberalisation, trade policy is once again being used to safeguard domestic industries, and supply chains are being reconfigured to favour strategic allies (see Figure 5).

Figure 5: World value of exported goods and services as a share of GDP, 1970-2023 (per cent)

Source: Aviva Investors, World Bank Group, 2023.3

Security and resilience are also front and centre of government concerns. Nations are increasingly prioritising defence, but also energy security, data security, and protecting against non-traditional threats such as cyber-attacks.

Political and social factors are contributing to the evolving geopolitical landscape, from the effects of social inequality and housing shortages to the rise of nationalism and populism in politics, and issues around migration, displacement and global mobility.

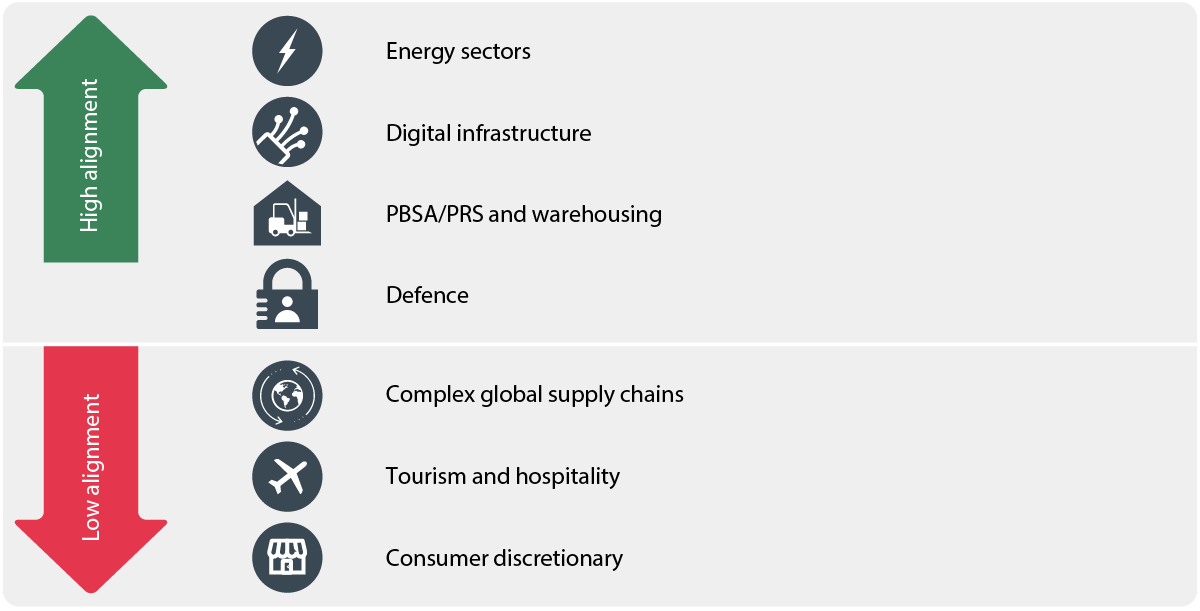

Figure 6: Sectors most and least aligned to the new global order

Source: Aviva Investors, as of May 2025.

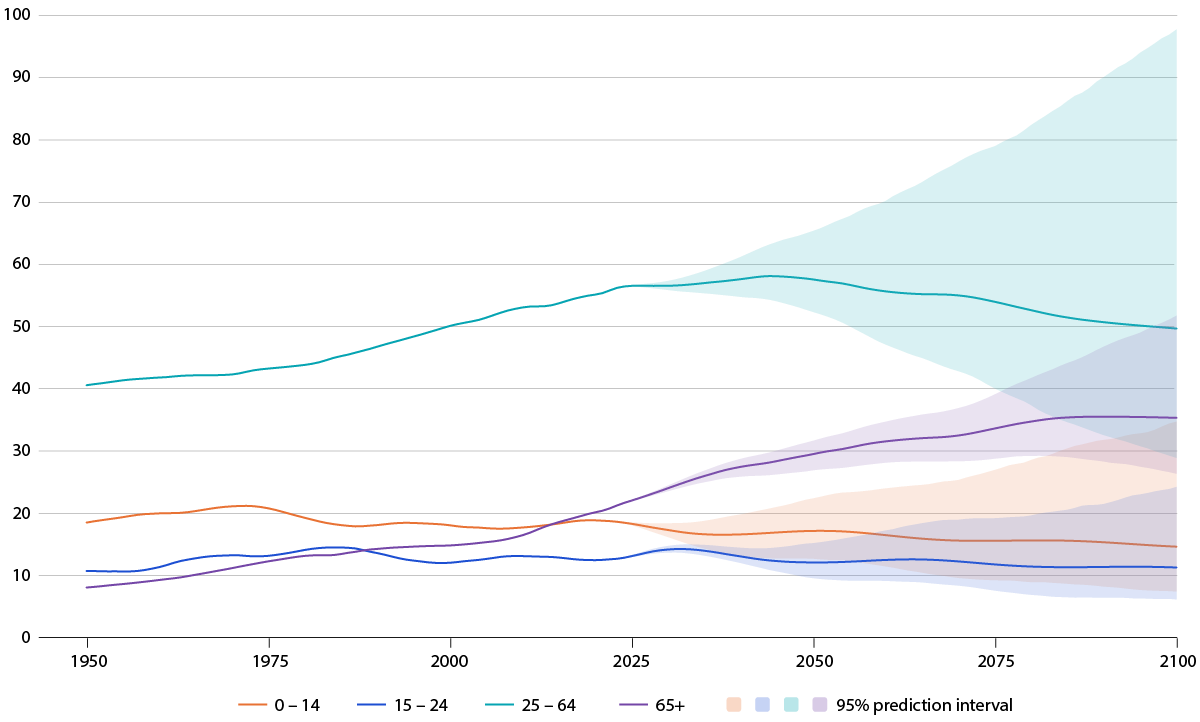

“D”: Demographics

Increased life expectancy but lower birth rates mean populations are still growing, but also aging (see Figure 7). This is leading to evolving societal needs, transforming housing demand and introducing new economic challenges as working-age populations shrink relative to pensioners – though this varies by region.

Figure 7: Northern Europe population by age group, 1950-2100 (in millions)

Source: Aviva Investors, United Nations.4

Across emerging markets, the growth of the middle classes is also transforming economies and consumer demand. Globally, other population trends and preferences are also changing or reinforcing. Urban migration, digital engagement and digital living are gaining momentum, as are preferences towards single-person households, sustainability and eco-friendliness.

Figure 8: Sectors most and least aligned to demographic changes

Source: Aviva Investors, as of May 2025.

MegaTRENDs: hard to quantify, but not to be ignored

Having refined these trends, the private markets team has analysed and assessed their potential impact and given sub-asset classes an alignment score for each trend. These scores are based on a combination of quantitative and qualitative factors as well as expert opinion over a ten-year time horizon and apply to debt and equity investments for European private markets. The TRENDs thus offer a larger framework for incorporating long-term sector risk assessments when thinking about private market investments as well as portfolio construction.

MegaTRENDs are just one part of a broader evaluation

MegaTRENDs serve as a valuable consideration within our investment process, but they are just one part of a broader evaluation. Crucially, we also emphasise the importance of asset-level specifics, which play a decisive role in shaping the risk-return profile given the heterogenous nature of private market investments.

A low score means the trend is more of a headwind or risk to investments, neutral means there could be offsetting risks on both the upside and downside, and a high score means the trend presents more opportunities than risks. In addition, all the scores are relative to each other. Each desk has therefore calibrated its TREND scoring across asset classes (see Figure 9).

Figure 9: TRENDs in private markets

Source: Aviva Investors, as of May 2025.

The framework reveals what strategies and sectors may be most aligned to the megatrends, such as prime city offices in real estate, renewable energy infrastructure and information technology sectors.

The TRENDs framework is one of many useful inputs into broad sector views and high-level risk-reward assessments

But it can also indicate where future risks might lie, enabling investors to mitigate them through investment decisions and portfolio construction. In real estate, for instance, secondary offices, retail and leisure all show low alignment to the megatrends. Investors in those sectors should be extremely selective at asset level, and the long-term risks could require a higher risk premium.

The interplay between TRENDs, sectors and investment practices is complex and dynamic, and many sub-asset classes align to some of the megatrends but not others. For example, life sciences score highly on technology and demographics, as investing in pharmaceutical laboratories supports the development of drugs like vaccines or new cancer treatments. However, these laboratories are energy hungry, mainly due to their stringent requirements to maintain sterile environments and avoid contamination. Investors need to square the circle of positives and negatives through financial and risk-reward analysis at asset level.

The TRENDs framework is therefore one of many useful inputs into broad sector views and high-level risk-reward assessments. By assessing these deep, long-term influences and their dynamics, investors can identify attractive opportunities and reap financial rewards.